Debt can be one of the biggest obstacles to building wealth. High-interest loans, credit cards, and personal loans can drain your income, slow down savings, and create financial stress. Paying off debt efficiently allows you to regain control, reduce interest costs, and accelerate your path to financial freedom.

Why Paying Off Debt Quickly Matters

- Save on Interest: The longer debt remains, the more interest you pay. Faster repayment reduces overall cost.

- Increase Financial Flexibility: Fewer debts free up income for savings, investments, or emergencies.

- Reduce Stress: Debt can cause anxiety and limit lifestyle choices. Paying it off improves mental well-being.

- Accelerate Wealth Building: Money that would go to interest can instead grow in investments.

Step 1: Know Your Debt

List all your debts including:

- Credit cards

- Personal loans

- Student loans

- Car loans

Include the balance, interest rate, and minimum monthly payment for each. This gives a clear picture of where you stand.

Step 2: Choose a Repayment Strategy

There are two popular strategies for paying off debt faster:

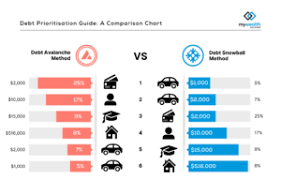

- Debt Avalanche Method:

- Focus on paying off the debt with the highest interest rate first.

- Make minimum payments on all other debts.

- Once the highest-interest debt is gone, move to the next highest.

- Pros: Saves the most money on interest over time.

- Debt Snowball Method:

- Focus on paying off the smallest debt first.

- Make minimum payments on larger debts.

- Once the smallest is paid, move to the next smallest.

- Pros: Provides quick wins and motivation.

Choose the method that suits your personality and keeps you motivated.

Step 3: Increase Your Payments

Even small extra payments can significantly reduce debt over time. Strategies include:

- Directing windfalls (bonuses, tax refunds) toward debt

- Cutting non-essential expenses to free up cash

- Using side hustle income to pay down balances faster

Step 4: Lower Interest Rates Where Possible

High-interest debt slows repayment. Explore ways to reduce interest:

- Transfer balances to lower-interest credit cards

- Consolidate debt into a lower-rate personal loan

- Negotiate lower rates with lenders

Reducing interest helps you pay off debt faster and save money.

Step 5: Automate Payments

Set up automatic payments to ensure consistency and avoid late fees. Regular, on-time payments reduce stress and prevent credit score damage.

Step 6: Avoid Accumulating More Debt

While paying off existing debt, avoid creating new debt. Use cash or debit cards for purchases and practice disciplined spending habits.

Step 7: Track Progress

Regularly monitoring your debt reduction progress keeps you motivated and helps adjust strategies if necessary. Seeing balances shrink over time reinforces positive habits.

Step 8: Focus on Lifestyle Adjustments

Small lifestyle changes can free up money for debt repayment:

- Limit dining out or subscriptions

- Reduce unnecessary shopping

- Use public transport or carpooling

- Sell unused items for extra cash

Step 9: Build an Emergency Fund Simultaneously

While repaying debt, maintain a small emergency fund to avoid relying on credit during unexpected expenses. Even $500–$1,000 can prevent setbacks.

Step 10: Celebrate Milestones

Acknowledging achievements, such as paying off a credit card or loan, keeps motivation high and encourages continued progress.

Common Mistakes to Avoid

- Paying only the minimum amount due

- Ignoring interest rates when prioritizing debt

- Taking on new debt while repaying old debt

- Not tracking spending and payments

Final Thoughts

Paying off debt faster requires discipline, planning, and consistent effort. By using structured repayment strategies, increasing payments, reducing interest, and avoiding new debt, anyone can regain financial freedom faster.

Debt repayment is not just about numbers—it’s about creating space for savings, investments, and long-term wealth-building. The sooner you start, the sooner you can redirect your money toward growing your financial future.